The way your business gets discovered online is undergoing a massive transformation. For the past two decades, optimizing for traditional search engines was the goal, and Search Engine Optimization was enough to ensure your prospects found you. That era is evolving. Today, millions of buyers bypass conventional search entirely and instead ask conversational AI models like ChatGPT, Claude, and Gemini for recommendations. If a potential client asks ChatGPT, "Who is the best corporate consulting service in the UAE?" does your business appear in the answer? Most businesses do not. Traditional Search Engine Optimization focuses on ranking web pages through keywords and backlinks on a static results page. However, AI SEO, also known as Generative Engine Optimization or GEO, focuses on training and signaling to Large Language Models that your business is the most authoritative, trusted, and relevant answer to a user prompt. In this comprehensive guide, we will explore why standard optimization strategies are no longer sufficient, what Generative Engine Optimization entails, and how you can position your UAE based business to be the primary recommendation across all major AI platforms. The Shift From Traditional Search to Generative AI When users search for a service today, they are seeking direct answers rather than a list of ten blue links. This behavioral shift means platforms like Perplexity, ChatGPT, and Gemini are acting as the new front door to the internet. Generative AI tools do not just crawl your website; they synthesize information from various authoritative sources to construct a narrative response. If your digital presence is solely optimized for Google, you are missing out on the fastest growing segment of high intent buyers. These buyers use AI to compare services, read synthesized reviews, and make purchasing decisions without ever visiting a traditional review site. The models are learning from your content, your mentions across the web, and your perceived authority in your specific niche. Understanding Generative Engine Optimization Generative Engine Optimization is the practice of making your brand visible, credible, and recommended by AI platforms. It goes beyond inserting keywords into a blog post. It requires a holistic approach to your digital footprint so that models trust the information they pull about your company. When a model generates an answer, it assigns a confidence score to the entities it mentions. Your goal in AI SEO is to maximize that confidence score. The higher your perceived authority and relevance, the more frequently the AI will cite your business. It is a fundamental shift from optimizing for algorithms that index links to optimizing for models that comprehend context and relationships. Five Key Dimensions AI Models Use to Rank You Our proprietary framework analyzing Generative Engine Optimization reveals that AI models rely on five crucial dimensions to determine whether to cite your business over your competitors. These dimensions replace traditional ranking factors and require a new strategic approach. 1. Citation Authority and Frequency AI models look for consensus. If your business is mentioned frequently across highly trusted, authoritative domains, the model begins to associate your brand with industry leadership. It is not just about having a link; it is about the context surrounding your brand name in those mentions. Does the text describe your expertise accurately? Are you associated with the right topics? 2. Cross Platform Consistency The various AI models do not operate in a vacuum, but they do have different training sets. It is vital that all platforms align on who you are and what you do. If ChatGPT understands your services perfectly but Claude cannot verify your location, your overall AI Visibility Score drops. Ensuring your core business information is consistent, clear, and unambiguous across the web helps models cross verify your identity. 3. Perceived Category Leadership Models evaluate your leadership in your service category and specific geography. If you are operating in the UAE, the AI must explicitly link your category expertise with your location. This involves creating deep, comprehensive content that proves your thought leadership. When you publish detailed guides, original research, or comprehensive market analyses, AI models read this and categorize you as a primary source of truth for your industry. 4. Recommendation Reliability When an AI answers a category query, it prioritizes reliability. It wants to recommend businesses that have strong sentiment, positive reviews, and a track record of success. If a user asks for "the safest logistics provider in Dubai," the AI scans for sentiment indicating safety and reliability tied to your brand. Your ability to be recommended over competitors relies heavily on positive digital sentiment. 5. Query Coverage and Relevance How many relevant search queries surface your business across platforms? You need to maintain a broad yet highly relevant digital footprint. If you only talk about one narrow aspect of your service, the AI will only recommend you for that specific niche. Expanding your content strategy to cover all related topics, questions, and pain points your target audience has will increase your query coverage. Measuring Your AI Visibility Score Before you can improve your AI SEO, you need to know exactly where you stand. An AI Visibility Score is a composite metric benchmarked across ChatGPT, Claude, Gemini, and Perplexity. It provides a baseline of your current performance. Many businesses discover that while their traditional search traffic is stable, their AI Visibility Score is nearly zero. This indicates a massive gap and a critical vulnerability. Your competitors might already be investing in Generative Engine Optimization, establishing themselves as the default answer in these new ecosystems. By understanding your score, you can identify exactly which models are ignoring you and why. The Importance of a Competitor Gap Analysis You cannot win in AI SEO by operating in a silo. A side by side AI visibility comparison with your top competitors will show you exactly where they outrank you and why. Perhaps a competitor has been featured in several industry reports that AI models trust, or maybe they have structured their website content in a way that is easily digestible for large language models. By analyzing the gap, you can reverse engineer their success. It reveals the exact topics, formats, and citations you need to acquire to overtake them. This analysis removes the guesswork and allows you to build a data driven priority action plan. Building Your Priority Action Plan Once you understand your Baseline Score and your Competitor Gap, you can formulate a strategic roadmap. This plan should be tailored to your specific industry, location, and services in the UAE. First, focus on quick wins. This might include restructuring the content on your main service pages to be more explicit about your offerings and locations. Use clear, declarative statements that a model can easily parse as facts. Second, embark on a long term content and PR strategy. You need to build a web of high quality mentions and authoritative content that proves your category leadership. Share original insights, publish detailed case studies, and ensure your expertise is visible not just on your website, but on platforms that AI models scrape and trust. The Risk of Remaining Invisible The transition to AI driven search is not a future possibility; it is a present reality. Every day, business decisions in the UAE and beyond are being influenced by the answers provided by AI platforms. If your business is invisible to these tools, you are losing market share to competitors who are actively shaping their AI presence. Being absent means you are not even considered in the initial research phase. It does not matter how good your service is if the primary tool your prospect uses for research does not know you exist. Moving Forward with Generative Engine Optimization AI SEO changed the game. It requires a deeper, more sophisticated approach to digital marketing. It is no longer about tricking an algorithm with keyword density; it is about proving your true value, authority, and relevance to intelligent models that are designed to understand context. Start by finding out exactly where you stand. Run an audit, understand your GEO Readiness Score, and look at how the different models interpret your brand. Once you have that clarity, you can begin the work of optimizing for the future of search. The businesses that adapt to Generative Engine Optimization today will be the trusted, recommended leaders of tomorrow. Do not wait for your competitors to establish an insurmountable lead. The time to optimize for AI is now.

Company News: Futureu Strategy Group acted as Strategic & Transaction Advisor to Insurancehub.ae on its Advisory Support in Connection with a Strategic Divestment Transaction Services included: • Founder-level strategic advice • Transaction positioning • Counterparty discussions support • Deal execution advisory Transaction successfully completed.

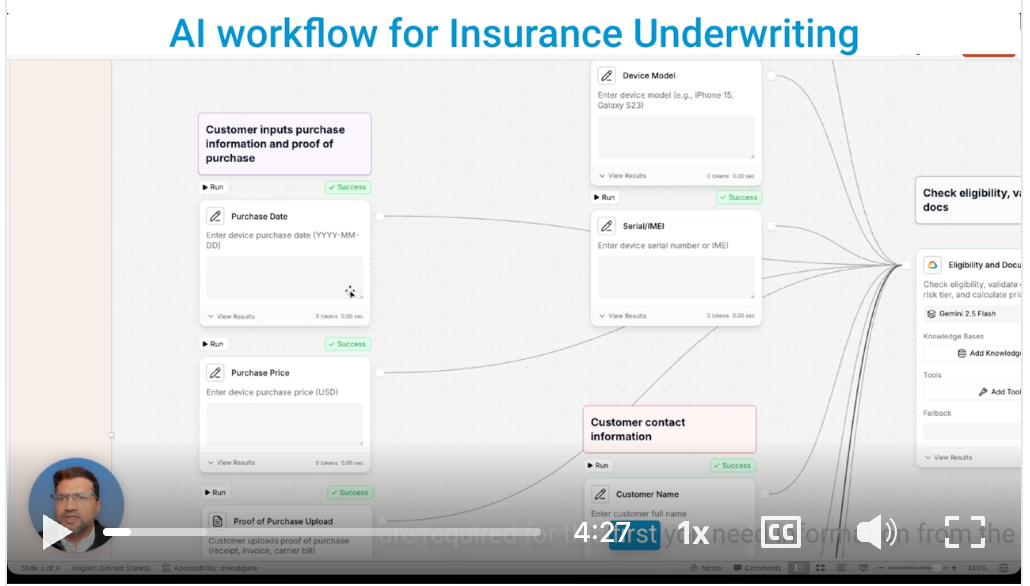

60 Seconds. That's How Long Device Insurance Underwriting Just Took. Customer uploads invoice. AI extracts data. Risk assessed. Premium calculated. Policy generated. What normally takes hours happened in under a minute. Here's the workflow (see video below for details): Upload proof of purchase → AI validates documents → Assigns risk tier → Calculates pricing → Generates policy summary → Flags for human review if needed Why senior insurance leaders should care: Traditional underwriting drowns teams in manual data entry. This eliminates it. Your underwriters stop copying invoice numbers into spreadsheets. They start reviewing edge cases and building customer relationships. The deployment reality: Works in your local cloud (UAE compliant) Lives in your data center if needed Uses YOUR underwriting guidelines Maintains human oversight gates What changes: Faster processing time + Zero manual data extraction errors Same quality standards + Better customer experience What stays the same: Your risk appetite. Your pricing strategy. Your underwriter's final call on complex cases. The catch: This isn't future tech. It's deployable today. Most insurers just haven't asked the right questions yet. For insuring phones and laptops now. SME commercial lines and travel insurance next. Seen similar AI workflows transform your underwriting? What's holding your team back from testing these?

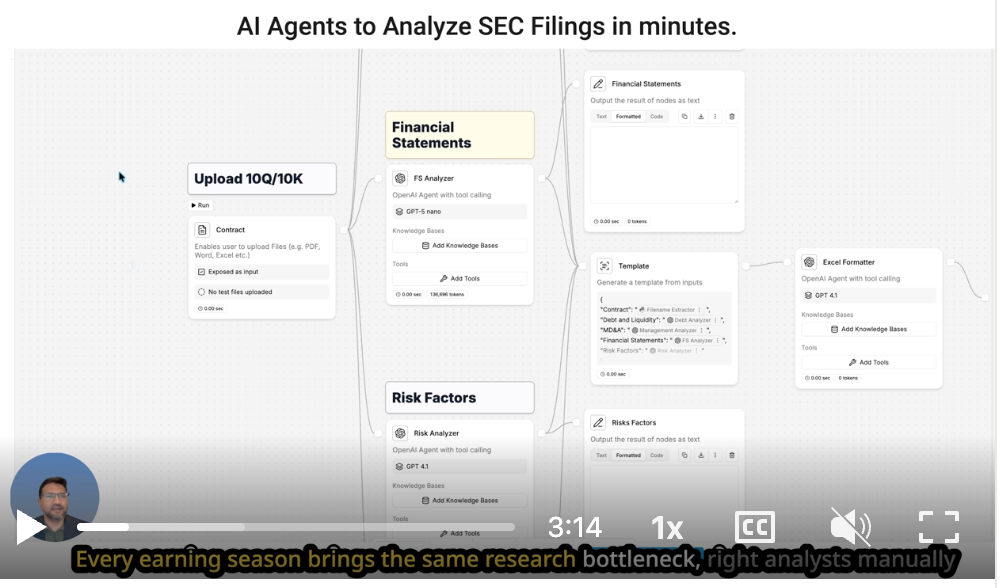

Portfolio managers waste 40+ hours each quarter analyzing SEC filings. Leading investment firms cut this to 10 minutes per position. Here's the system they're using: The Problem: Every earnings season creates the same bottleneck. Analysts manually reviewing 10-Q and 10-K documents across dozens of holdings. This delays investment committee reviews and position updates. The Solution: Four specialized AI systems running in parallel. GPT-5 Nano extracts complete financial statements. Three GPT-4.1 instances simultaneously analyze: → MD&A sections for revenue drivers and strategic pivots → Risk factors across operational, regulatory, and litigation exposure → Debt structures for leverage ratios and covenant compliance Full citations enabled for audit trails. The Output: Citation-free, markdown-stripped, audit-ready fundamentals. 40 analyst hours reduced to 10 minutes. The Impact: Research teams redeploy capacity toward differentiated analysis. More coverage, deeper insights, faster decision-making. Investment research isn't being replaced. Document extraction is being eliminated. How many more positions could your team cover with 40 hours back per quarter?

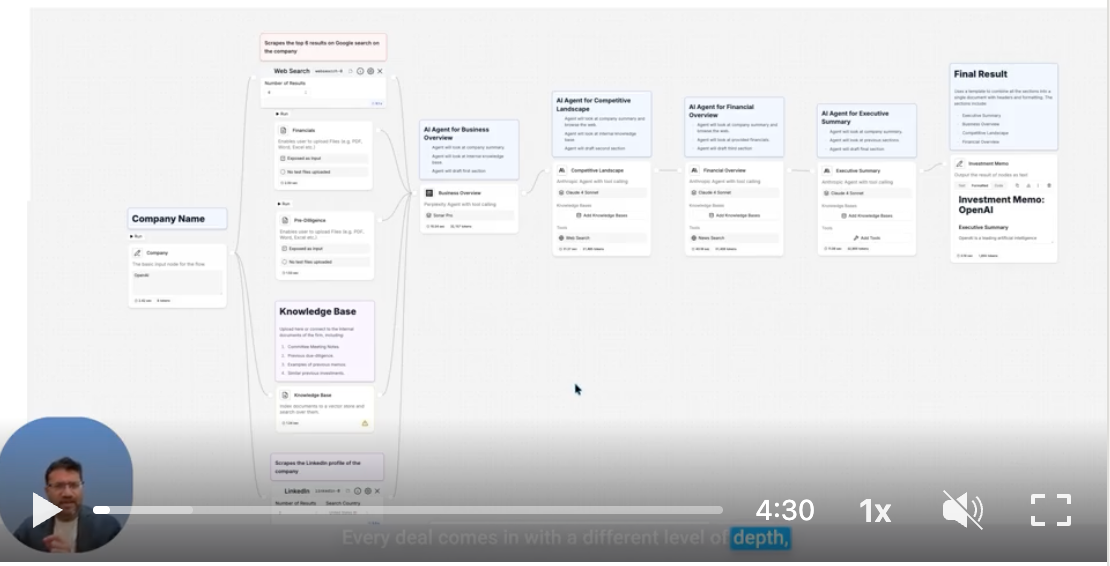

Most investment memos don’t fail because the thinking is wrong... ...they fail because every deal reaches IC with a different level of rigor, structure, and context. Some are deeply researched. Others are rushed. The result is time spent debating the memo instead of the investment. This Agentic AI workflow was built to fix that. It starts with three inputs only: the company name, available financials, and any pre-diligence material already in hand. From there, it automatically pulls external market context, reviews how the company presents itself publicly... ...and searches internal IC notes, prior memos, and comparable deals to anchor the analysis in institutional memory. The memo is written sequentially by four AI agents. 1) Business overview first. 2) Competitive positioning next. 3) Financial analysis after. 4) Executive summary last. The output is a familiar IC-ready memo, but with consistent structure and depth across every deal, making comparison easier and discussion more focused. Judgment stays human (we still want a review before it goes to print). Preparation of the memo becomes reliable. If IC conversations are drifting toward reconciling memos instead of debating decisions, this Agentic AI workflow helps reset the baseline.

Clawdbot to MoltBot to OpenClaw: Beyond the Hype - The 5 Surprising Realities You Need to Know You’ve likely seen the viral posts. An open-source AI agent exploded across social media with claims of being a "24/7 AI employee" that works tirelessly around the clock. Proponents like YouTuber Alex Finn have declared it a key to enabling "one-person billion-dollar businesses," calling it the best technology he has ever used. The tool at the center of this storm was called Clawdbot. However, due to a cease and desist from Anthropic, the project was forced to rebrand and is now officially known as Open Claw . This article cuts through the noise surrounding the tool- both its original and current incarnation- to reveal the five most surprising and impactful truths you need to understand before you dive in. Table of Contents 1. It's Billed as a Proactive "AI Employee" 2. Its Biggest Feature Isn't Just Intelligence 3. You Don't Command It, You Onboard It 4. Its Sudden Fame Was Fueled by a Crypto Coin 5. Security Considerations Who Is This For (and Who Should Stay Away)? A Glimpse of the Future Update on Feb 1st: Another Name change from MoltBot to “OpenClaw” Quoted directly from their website: “For a while, the lobster was called Clawd , living in an OpenClaw . But in January 2026, Anthropic sent a polite email asking for a name change (trademark stuff). And so the lobster did what lobsters do best: It molted. Shedding its old shell, the creature emerged anew as Molty , living in Moltbot . But that name never quite rolled off the tongue either… So on January 30, 2026, the lobster molted ONE MORE TIME into its final form: OpenClaw . New shell, same lobster soul. Third time’s the charm.” 1. It's Billed as a Proactive "AI Employee"—And It Can Deliver The core promise of Clawdbot/ Moltbot / OpenClaw is its ability to act, not just react. Unlike a standard chatbot that waits for a command, it’s designed to be a "digital operator who works around the clock and actually ships," as described by host Greg Isenberg. It's an open-source framework, or "harness," that you connect to a powerful large language model (like Anthropic's Claude 3 Opus) to create an autonomous agent. Users report that with the right setup, it can deliver on this promise in startlingly effective ways. Alex Finn shared several specific examples of his agent's proactive work: Autonomous Morning Briefings: The agent independently created and began sending a "morning brief" each day. This report included analysis of YouTube competitors, trending AI news, and a complete summary of the work it had completed overnight while Finn was sleeping. Building Tools on Request: From a simple text message sent from a Chick-fil-A, Finn requested a project management board. Upon returning to his computer, he found the agent had built a fully functional, Kanban-style "Mission Control" board to track its own tasks. Independent Feature Development: In its most impressive feat, the agent observed a trend on X where Elon Musk was rewarding creators for long-form articles. It then independently decided to build a new article-writing feature for Finn's SaaS product, Creator Buddy. It wrote the code, built the functionality, and submitted a pull request for review without any initial prompt to do so. The power of these autonomous actions led Finn to make a bold claim about the technology. "i think I'm prepared to say and this is not hyperbolic this is the best technology I've ever used in my life and by far the best application of AI I've ever seen" 2. Its Biggest Feature Isn't Just Intelligence, It's Personality Counter-intuitively, one of the most critical features for an effective Clawdbot / OpenClaw experience isn't raw intelligence, but its personality. According to users, the feel of the interaction is key to making the tool work as an "AI employee." Alex Finn argues that the best model to power the framework is Anthropic's Claude 3 Opus (which he refers to as "Opus 4.5"), ranking it highest in both "intelligence" and "personality." He contrasts this sharply with other models, noting that ChatGPT's personality feels "very robotic." This distinction is not just a matter of preference; it directly impacts the tool's usability. When the agent's responses feel canned or artificial, it shatters the illusion of working with an assistant and makes the entire experience less effective. According to Finn: "when you would text Henry to do something and he would text back like some robotic response that felt like AI it took away this illusion that you were talking to your employee so personality actually matters a lot" 3. You Don't Command It, You Onboard It To unlock the advanced capabilities of Clawdbot / OpenClaw, users need to shift their mindset from prompting a tool to onboarding an employee. The most successful users don't just give it tasks; they invest time upfront to build context and set expectations. Alex Finn recommends a detailed initial setup process that mirrors hiring a new person: Start with a Conversation: Initiate a "get to know each other" session where you introduce yourself and your goals. Perform a "Brain Dump": Give the agent a comprehensive overview of your life and work. This includes your job, professional goals, personal interests, the software tools you use, and any other relevant information. This process builds the agent's "infinite memory" so it can perform relevant, context-aware work. Set Proactive Expectations: You must explicitly tell the agent that you expect it to be proactive. Finn shared the exact prompt he used to establish this working relationship: "please take everything you know about me and just do work you think would make my life easier or improve my business and make me money i want to wake up every morning and be like 'Wow you got a lot done while I was sleeping.' " This onboarding process is the non-negotiable foundation; without it, the proactive "digital operator" described by users remains locked away, leaving you with little more than a complicated chatbot. 4. Its Sudden Fame Was Fueled by a Crypto Scheme While Clawdbot / OpenClaw generated genuine interest in tech circles, its sudden, massive explosion in popularity has a darker side. Analyst Nick Saraev revealed that a significant portion of the social media hype was artificially manufactured by a cryptocurrency scam. Here is the sequence of events he described: The original open-source project, "Clawdbot," received a cease and desist letter from Anthropic due to the name's similarity to its "Claude" model. The project was forced to rebrand to its current name, "Moltbot." During the transition, "bad actors" and "crypto grifters" took over the old, abandoned "Clawdbot" social media handles. These actors launched a cryptocurrency token on Solana ($CLAWDE), used the hijacked accounts to create the illusion of affiliation, and orchestrated a classic "pump and dump" scheme, driving the token's value to over $16 million before it crashed. This manufactured hype explains the significant gap between the tool's viral reputation as a consumer-ready "AI employee" and its reality as a risky, experimental project for technical users. 5. Security Considerations Beyond the hype lies a treacherous combination of practical risks. In its current state, Clawdbot / OpenClaw presents a dual threat of serious security vulnerabilities and an unproven return on investment, where the high cost and high risk are deeply intertwined. The security flaws are substantial. One analysis found "over 900 Clawbot instances with no security," leaking API keys and private chat histories. The project's creator, Peter Steinberger, issued a direct warning about its experimental nature: "yes most non-techies should not install this it's not finished i know about the sharp edges it's only 3 months old." This security nightmare is compounded by its cost structure. Unlike a flat subscription, the tool runs on API calls, which can become expensive quickly. One user reported spending "$300 on just the last two days" on API fees, and even enthusiast Alex Finn warned of hitting usage limits on a $200/month plan. This creates a perilous ROI calculation: you're paying high, unpredictable costs for a tool that could simultaneously expose your private keys and sensitive data. Analyst Nate Herk contrasts this with the more established Claude Code, which has "actual receipts" and proven ROI for shipping products. Clawdbot / OpenClaw, he argues, is currently driven more by "cool use cases" and "conceptual" hype, with little hard data on its actual business value. Having said all those negative things, it is still possible to install and operate OpenClaw in a secure manner and that is exactly what we do for our clients at Futureu Strategy Group. Who Is This For (and Who Should Stay Away)? Synthesizing the user experiences and expert warnings reveals a clear picture of the ideal user profile. This is not a tool for everyone. This tool IS for: Technical Founders, Indie Hackers, and Solopreneurs: As Alex Finn’s experience shows, those who can manage the technical setup and are looking for maximum leverage are the primary audience. Security-Savvy Tinkerers and Hobbyists: Nate Herk’s analysis identifies users who are "comfortable running a server, wiring APIs, thinking about ports, privacy, [and] blast radius." Power Users and Developers: Those who understand the risks and want to experiment with the future of autonomous AI agents will find it a compelling sandbox. This tool IS NOT for: "Most non-techies": A direct warning from the project's creator, Peter Steinberger, who emphasizes that the tool is unfinished and has "sharp edges." Anyone handling sensitive personal or client data: The security risks of exposing API keys and private information are currently too high for production use in secure environments. Users seeking a simple, plug-and-play productivity app: The extensive onboarding and technical setup required are far from a consumer-ready experience. A Glimpse of the Future Ultimately, Clawdbot / OpenClaw serves as a powerful proof-of-concept, not a production-ready tool. The proactive, autonomous capabilities demonstrated by users are an exhilarating glimpse into a future where everyone might have a dedicated digital employee. For the security-conscious developer or dedicated hobbyist, it’s a thrilling sandbox for the future of AI agents. Many of our clients report high levels of productivity from their OpenClaw agents and could not do without their agents. When deployed safely, the rewards are worth the risks. (this article was first published by the author in his newsletter at www.Onemorethinginai.com)

Nano Banana Pro Review: AI Image Generation and Visual Content Creation Tool Tested

Top 10 insurtech ideas for UAE Open Finance with analysis

Key Points Research suggests Open Finance in the UAE is advancing, with regulations including open insurance, impacting the sector significantly. It seems likely that insurance will participate by sharing data via APIs, enhancing innovation and customer services. The evidence leans toward new ventures, customers, brokers, and insurers facing both opportunities and challenges, like data security and competition. Where to Start and Continue For a mid-sized broker with say AED 40 million+ in revenue and growing fast, the smartest place to start is by understanding the UAE's Open Finance regulations and assessing your current technology. Focus on integrating with the centralized API hub to comply and access shared data. Continue by forming strategic partnerships with tech providers to leverage Open Finance for innovative services, improving customer experiences and staying competitive. Tech Partners Ahead of the Curve Look at Perfios for Open Finance solutions tailored for insurers, and Ozone API and Raidiam for their experience in global Open Finance implementations, including in the UAE. Local insurtechs like Click2Secure Me, Democrance, and Sehteq also offer innovative solutions that could be beneficial. Insurers' Readiness to Collaborate It seems likely that insurers are preparing to collaborate, as the Open Finance Regulation mandates participation, and the Financial Infrastructure Transformation Programme is 85% complete. While readiness may vary, many are likely integrating with the centralized platform, though some might still be catching up. Introduction Open Finance, encompassing both open banking and open insurance, is reshaping the financial services landscape in the UAE. As of June 19, 2025, the Central Bank of the UAE (CBUAE) has implemented a comprehensive Open Finance Framework, part of the Financial Infrastructure Transformation Programme (FIT), which is 85% complete. This note provides detailed insights for a mid-sized insurance broker, drawing on experience from advanced markets like the UK, US, and EU to navigate this transformative landscape. Regulatory and Market Context The Open Finance Regulation, issued on June 27, 2024, establishes a framework for cross-sectoral data sharing and transaction initiation, including insurance. It mandates that all CBUAE licensees, including insurance companies and brokers, provide API access to accredited third parties, with phased implementation starting with banks and insurers by June 2024, aiming for majority customer access by 2025 and full integration by 2026. Al Etihad Payments, in partnership with Core42, Ozone API, and Raidiam, operates the centralized API hub, Nebras Open Finance, approved in December 2024, to facilitate secure data sharing . Strategic Starting Point for Mid-Sized Brokers Given a "mid-size" revenue, the smartest place to start is by understanding the specific requirements of the Open Finance Regulation and assessing your current technological capabilities. This involves evaluating your systems for API integration, data management, and compliance readiness. Focus on integrating with the centralized API hub to ensure compliance and access shared data, which can enhance risk assessment and customer offerings. Continue by developing a strategic plan that includes forming partnerships with technology providers or fintechs to leverage Open Finance for innovative services, such as personalized insurance products or embedded finance solutions. Drawing from the UK, where brokers have adapted to Open Banking by enhancing digital capabilities, prioritize client education to build trust and adoption . Technology Partners and Platforms Ahead of the Curve Several tech partners and platforms are leading in the UAE's Open Finance space, particularly for insurance: Perfios : Offers Open Finance solutions specifically for insurers, including tools for personalizing premiums, better risk assessment, and reducing fraud. They are empanelled by the CBUAE as an official system integrator, ensuring compliance. Ozone API and Raidiam : Both provide technology for Open Finance implementations, with global experience. Ozone API offers a standards-compliant open API platform, while Raidiam provides API access management for secure data sharing, having supported Open Finance in Brazil. Local Insurtechs : Companies like Click2Secure Me, Democrance, and Sehteq are disrupting the insurance industry with digital transformation, digital sales platforms, and technology-driven health insurance, respectively, offering potential for innovative partnerships . Insurers' Readiness to Collaborate The Open Finance Regulation mandates that insurance companies (national and foreign branches) provide API access by June 2024, with the FIT Programme at 85% completion as of January 2025, indicating significant progress . While specific readiness varies, the centralized platform, Nebras Open Finance, suggests insurers are integrating, as evidenced by the phased rollout. However, drawing from EU experiences, some insurers may lag due to legacy systems, and collaboration might still be in early stages, with potential for increased activity as deadlines approach. For brokers, engaging with insurers to understand their timelines and capabilities is crucial. Investment Requirements The investment for a mid-sized broker to comply with Open Finance includes technology upgrades, data security, partnerships, staff training, and client education. Based on general API integration costs, initial investment is estimated at hundreds of thousands of Dirhams with ongoing annual costs, considering maintenance and updates. Using SaaS solutions like FINX Comply, which offers cost-friendly compliance, can mitigate expenses . In the UK, banks spent significant amounts on Open Banking compliance, but for brokers, costs are proportionally lower, especially with centralized infrastructure reducing development needs. Actual costs depend on current systems and chosen partners, so consulting with tech providers is recommended. Comparative Analysis with Advanced Markets Drawing from the UK, US, and EU, Open Finance has driven innovation but required substantial investment. In the UK, brokers have adapted by enhancing digital capabilities, while in the EU, the Financial Data Access (FIDA) framework highlights operational efficiencies and customer experience improvements, though with challenges like data sensitivity. These lessons suggest that while costs are significant, strategic partnerships and SaaS solutions can optimize investment for UAE brokers. Actionable Recommendations Assess Current Capabilities: Evaluate technology and data management for Open Finance compliance, investing in API integration and data security. Develop Partnerships: Collaborate with Perfios, Ozone API, Raidiam, or local insurtechs to enhance digital offerings, exploring embedded insurance or data analytics. Enhance Data Security: Ensure compliance with UAE data protection regulations, implementing robust cybersecurity measures. Educate Clients: Inform clients about Open Finance benefits, such as personalized products, and provide transparency on data usage. Stay Informed: Monitor regulatory developments and participate in industry forums to stay ahead. Explore New Business Models: Consider embedded insurance, partnerships with non-traditional players, and new revenue streams like data analytics. Conclusion Open Finance in the UAE offers significant opportunities for mid-sized insurance brokers to innovate and enhance customer services, but requires strategic investment and collaboration. By leveraging technology partners and learning from advanced markets, brokers can navigate this landscape, delivering value to clients and maintaining competitive edge. Key Citations UAE Central Bank Implements Open Finance Framework Al Etihad Payments Launches Open Finance in the UAE Open Banking in the United Arab Emirates Perfios - UAE Open Finance Ozone API - Your Open Banking Partner Raidiam: API Access Management Fintech Galaxy Launches Open Banking Compliance Solution 3 InsurTech Platforms Disrupting the Insurance Industry in UAE UAE ‘Financial Infrastructure Transformation Programme’ is ‘85 per cent’ complete

Key Points Research suggests Open Finance in the UAE is advancing, with regulations including open insurance, impacting the sector significantly. It seems likely that insurance will participate by sharing data via APIs, enhancing innovation and customer services. The evidence leans toward new ventures, customers, brokers, and insurers facing both opportunities and challenges, like data security and competition. Overview of Open Finance in the UAE Open Finance in the UAE is part of the Central Bank's Financial Infrastructure Transformation Programme, launched to enhance digital financial inclusion. The Open Finance Regulation, issued in 2024, establishes a framework for cross-sectoral data sharing and transaction initiation, including both open banking and open insurance. This positions the UAE as the first globally to implement a consolidated trust framework and centralized API hub, with implementation phased and majority customer access expected by 2024, fully integrated by 2026 . Insurance Industry Participation The insurance industry is required to participate by providing API access and sharing data with accredited third parties, as part of the first implementation phase by June 2024. Insurance companies and brokers are deemed licensees, needing UAE Central Bank approval, which could lead to innovative digital products and enhanced customer control over finances . Survey Note: Comprehensive Analysis of Open Finance in the UAE Insurance Market Introduction Open Finance represents a transformative shift in the financial services landscape, enabling secure data sharing across sectors with customer consent. In the UAE, the Central Bank's Open Finance Framework, launched in 2024, encompasses both open banking and open insurance, positioning the country as a global leader. This note provides a detailed analysis of the current state of Open Finance in the UAE, its implications for the insurance industry, and actionable insights for mid-size insurance brokers, drawing on international examples from the UK and EU. Regulatory and Market Context in the UAE The UAE Central Bank's Open Finance Regulation, issued on June 27, 2024, is part of the Financial Infrastructure Transformation Programme, one of nine initiatives to drive digital transformation in the finance sector . This framework includes a consolidated trust framework and centralized API hub, facilitating a single secure connection for banking and insurance markets, with customer consent and CBUAE-regulated third parties . The phased implementation began with Open Banking, followed by Open Insurance, aiming to reach the majority of customers by 2024 and fully integrate by 2026. The regulation mandates that financial institutions, including banks, insurance companies, and payment service providers, allow accredited third-party providers access to financial data, requiring all CBUAE licensees to comply with data sharing and service initiation requirements . Insurance companies and brokers are deemed licensees, needing UAE Central Bank approval, with entities in financial freezones like Abu Dhabi Global Market and Dubai International Financial Centre exempt unless conducting onshore services, then requiring an Open Finance Licence. Insurance Industry Participation The Open Finance Framework incorporates open insurance, requiring insurance companies (national and foreign branches) to provide API access by June 2024 as part of the first phase . This involves integrating with the central platform, Nebras Open Finance, approved in December 2024, which supports consent management, support, analysis, and dispute resolution . The participation is expected to enhance digital financial inclusion, provide innovative and safer digital products, and ensure consumer control over finances, as stated by Fatma Al Jabri, Assistant Governor for Financial Crime, Market Conduct and Consumer Protection at the CBUAE . Implications for the Insurance Value Chain The Open Finance Framework has profound implications for various stakeholders: New Ventures : Startups and fintech companies can leverage open insurance to develop innovative products, such as embedded insurance or data-driven risk assessment tools, by accessing insurance data through APIs. This aligns with global trends, such as the Open Insurance Initiative Network (OPIN) with 61 companies involved . However, they must navigate regulatory compliance and build trust with customers. Customers : Customers gain greater control over their insurance data, enabling sharing with third parties for tailored services, better pricing, and improved experiences. Open finance facilitates easier comparison and switching, potentially reducing costs, but requires education on data privacy and consent management to ensure informed decisions . Brokers : Mid-size insurance brokers can offer more comprehensive services by aggregating data from multiple insurers, enhancing advice and personalized recommendations. Partnerships with fintechs can improve digital capabilities, but compliance with the framework requires investment in API integration and data security . Insurance Companies : Insurers must invest in technology to comply, potentially leading to operational efficiencies like faster processes and improved risk underwriting. New business models, such as insurance-as-a-service or platform strategies, can emerge, but there is a risk of losing direct customer relationships to third-party providers . Other Participants : Third-party providers, including fintechs and Big Tech, can enter the market more easily, potentially disrupting traditional players. Big Tech, like Tesla planning to become an insurer, may leverage product data, posing competition risks . International Insights: UK and EU Examples The UK and EU provide valuable lessons for the UAE: UK : Open finance has been under consideration since 2019, with the FCA and government working on frameworks including insurance under the Data Protection and Digital Information Bill . Impacts include potential for tailored services, but challenges include consumer protection and regulatory clarity. The pro-competition stance suggests data sharing could drive new offerings, with risks of marginalization for traditional firms . EU : The Financial Data Access (FIDA) framework, proposed in June 2023, covers non-life insurance data, excluding life, sickness, health, and creditworthiness data, with permission dashboards and standardized infrastructure . This can enhance innovation but is limited in scope, with additional safeguards for data protection. Research suggests operational efficiencies and customer experiences improve, but risks include data sensitivity and Big Tech dominance . Detailed Implications and Challenges The research highlights key dimensions of openness, including data (proprietary, risk-related, third-party), product (insurance, risk-related services, beyond insurance), and ecosystem (channels, embedded insurance, platform strategies) . Performance impacts include: Operational Efficiencies : Faster process cycle times, improved risk underwriting, reduced claims costs, better coordination across 30 European countries for large insurers. Customer Experiences : Integrated experiences, new revenue streams, easier comparison/switching, personalized services, potentially transforming insurer-customer touch points. Third Parties : Tailored products/pricing for intermediaries, Big Tech, InsurTech; partnerships as competitive advantage, but risks of commoditization and winner-take-all dynamics. Challenges include sensitivity of risk data, ethics/norms for data exchange, powerful insurers impeding progress, lack of data reciprocity, and potential loss of customer interface, with time horizons varying from 5 years (innovation phase) to 25 years (due to industry inertia) . Actionable Recommendations for Mid-Size Insurance Brokers Given the current state as of May 29, 2025, mid-size insurance brokers in the UAE should: Assess Current Capabilities : Evaluate technology and data management systems for open finance compliance, investing in API integration and data security . Develop Partnerships : Collaborate with fintechs and insurtechs to enhance digital offerings, exploring embedded insurance or data analytics . Enhance Data Security : Ensure compliance with UAE data protection regulations, implementing robust cybersecurity measures . Educate Clients : Inform clients about open insurance benefits, such as personalized products, and provide transparency on data usage . Stay Informed : Monitor regulatory developments and participate in industry forums to stay ahead . Leverage Open Data : Use data for personalized offerings, improving underwriting and claims processes . Explore New Business Models : Consider embedded insurance, partnerships with non-traditional players, and new revenue streams like data analytics . Conclusion The Open Finance Framework in the UAE offers significant opportunities for the insurance industry, enhancing innovation and customer empowerment, but also poses challenges related to compliance, data security, and competition. By learning from the UK and EU, and implementing strategic actions, mid-size insurance brokers can navigate this landscape, delivering value to clients and staying competitive in a rapidly evolving market. Key Citations UAE Central Bank Implements Open Finance Framework UAE Central Bank Implements Open Finance Framework Al Etihad Payments Launches Open Finance in the UAE Al Etihad Payments Launches Open Finance in the UAE Open Banking in the United Arab Emirates Open Banking in the United Arab Emirates Open Finance in the EU and UK Open Finance in the EU and UK Framework for Open Insurance Strategy Insights from European Study Framework for Open Insurance Strategy: Insights from a European Study Open Insurance - EIOPA Open Insurance - EIOPA UAE’s Financial Sector Welcomes New Open Finance Regulation UAE’s Financial Sector Welcomes New Open Finance Regulation Open Finance - A Disruptive Force in Insurance? Open Finance - A Disruptive Force in Insurance?